TLDR

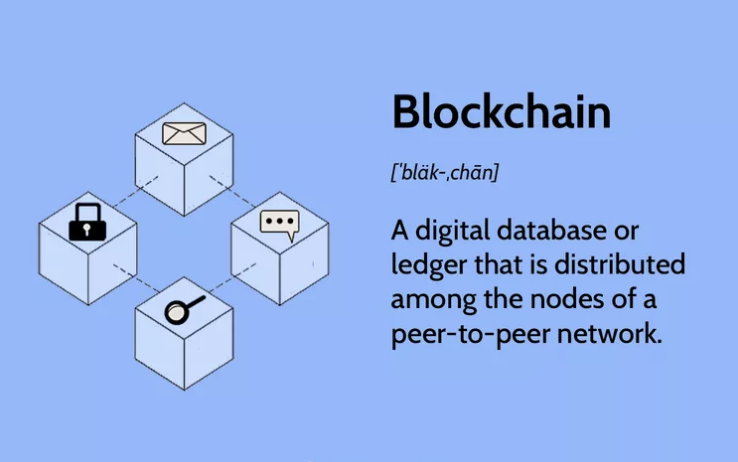

Blockchain is a technology that records and validates transactions in a digital ledger.

Users can employ it for financial transactions, as demonstrated by Bitcoin, or for other purposes like Ethereum’s smart contracts.

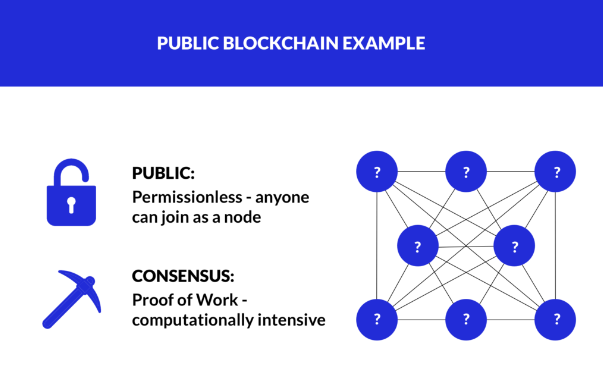

Blockchains cut the need for a central authority and use cryptography to secure transactions. Blocks store transactions and link together, forming a chain of records. Public blockchain networks are open to anyone, while private blockchains are only accessible to authorized users.

Blockchain technology can digitize any value, from a house to a car, and record ownership. Its uses extend to identity verification, political elections, and virtual reality.

What is blockchain?

In many contexts, people often associate blockchain technology with Bitcoin. Although blockchain technologies and Bitcoin are closely related, keeping the two separate is still essential. Blockchain has become a revolutionary wave of digital currency innovation and development, even independent of the cryptocurrency project it began with.

Companies worldwide in nearly every industry are adopting blockchain technology and eagerly searching for solutions to integrate existing services with blockchain systems. Enthusiasts firmly believe that this future technology will form the foundation for large parts of our society through blockchain systems and applications in the coming years.

Whether you are a technology enthusiast or want to invest in cryptocurrency, it’s wise to familiarize yourself with blockchain. This underlying technology is mainly responsible for decentralization in several sectors today.

This guide will go through blockchain, how it works in practice, and where the technology is heading. By acquiring the information, you will better understand how to make informed predictions and suitable investments.

How do programmers implement the design of blockchain technology?

Let’s begin by examining the programming of the blockchain and the underlying technological design of blockchain protocols.

The digital transaction ledger

The digital transaction ledger, often called the protocol, is the foundation of blockchain technology. In its simplest form, you can compare blockchain protocols to a massive Excel spreadsheet that records and validates all transactions on a specific chain.

This is also the original purpose of blockchain: to have a public and decentralized transaction ledger that does not rely on transaction fees or trust in an intermediary to conduct transactions.

Today, most economic transactions go through a bank or another payment provider. With this method, you have to pay transaction fees and trust that the bank or provider will perform the transaction as it should.

And yet, there are many challenges with these digital ledgers that record monetary transactions. Centralized systems are vulnerable to attacks and tampering. The transaction ledger on a blockchain is programming that is based on cryptography. To use the technology, you do not need to trust a person or financial institution; you need to trust math and cryptography.

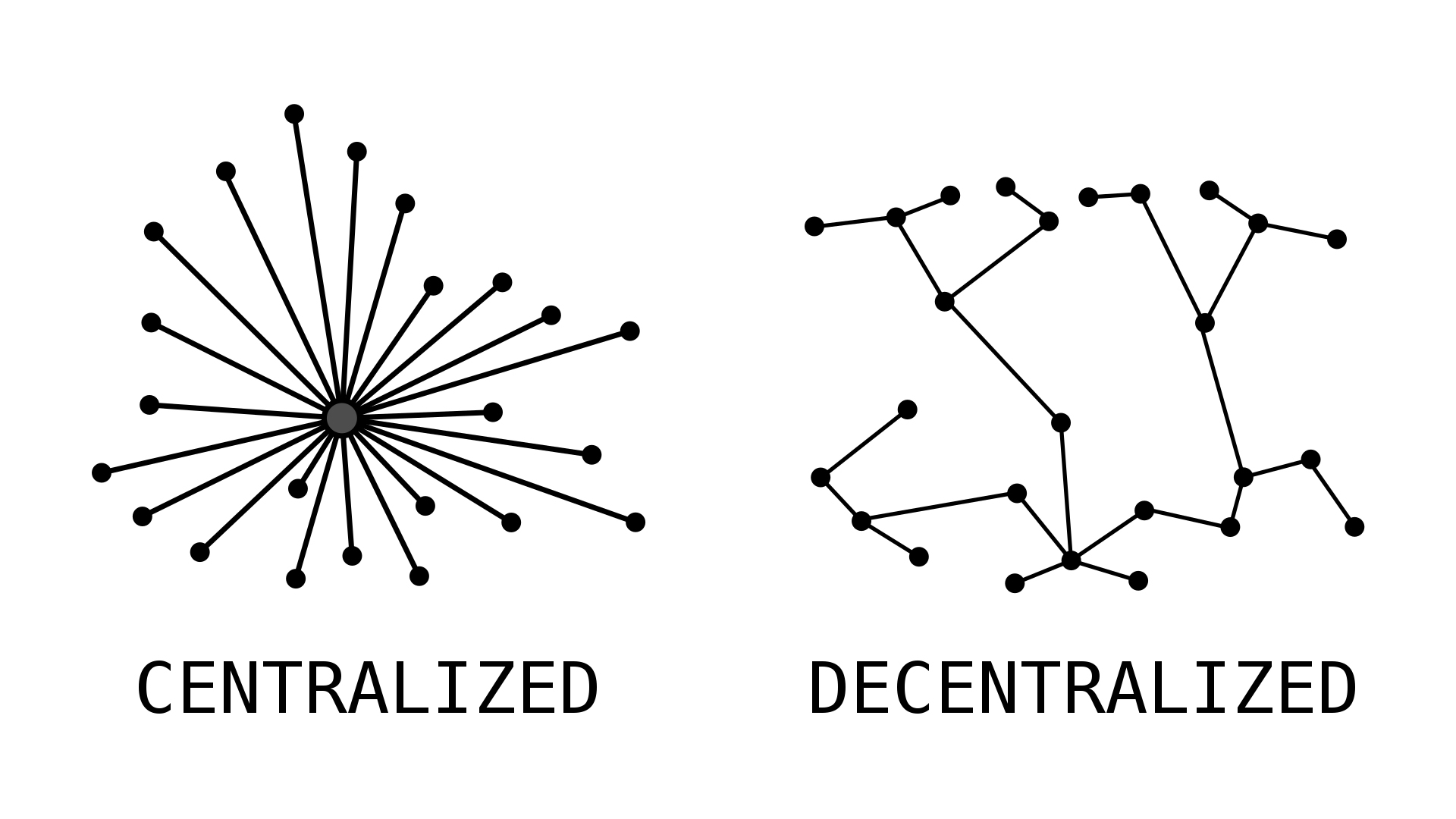

The decentralization and public nature of the information in the various transaction records and ledgers make blockchain technology special. From a security perspective, the consequence is that you cannot break a blockchain. But let’s go through exactly how a blockchain records this vast “Excel sheet” for recording transactions available to the world.

100% decentralized and public information

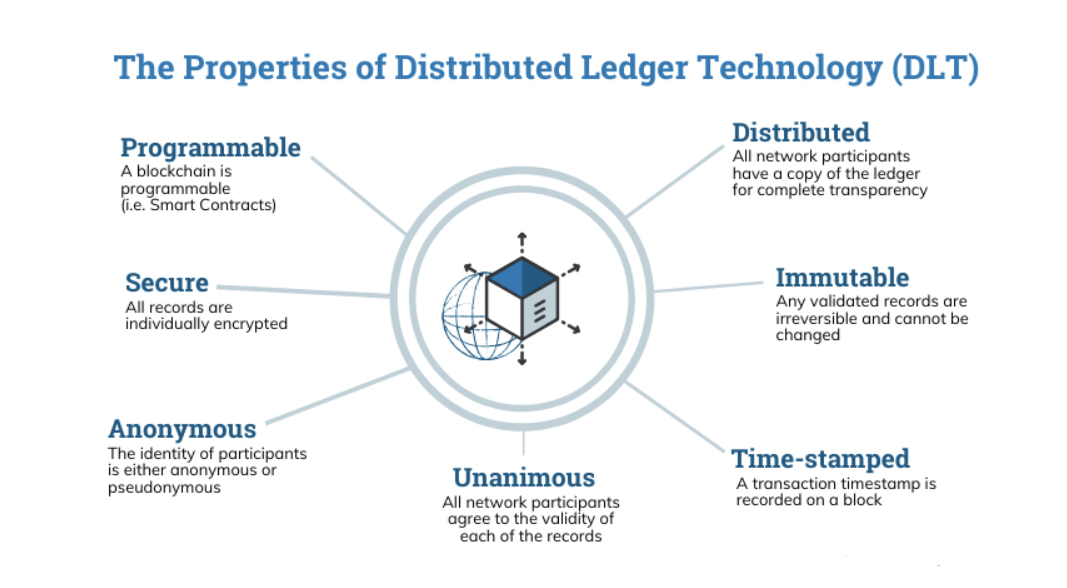

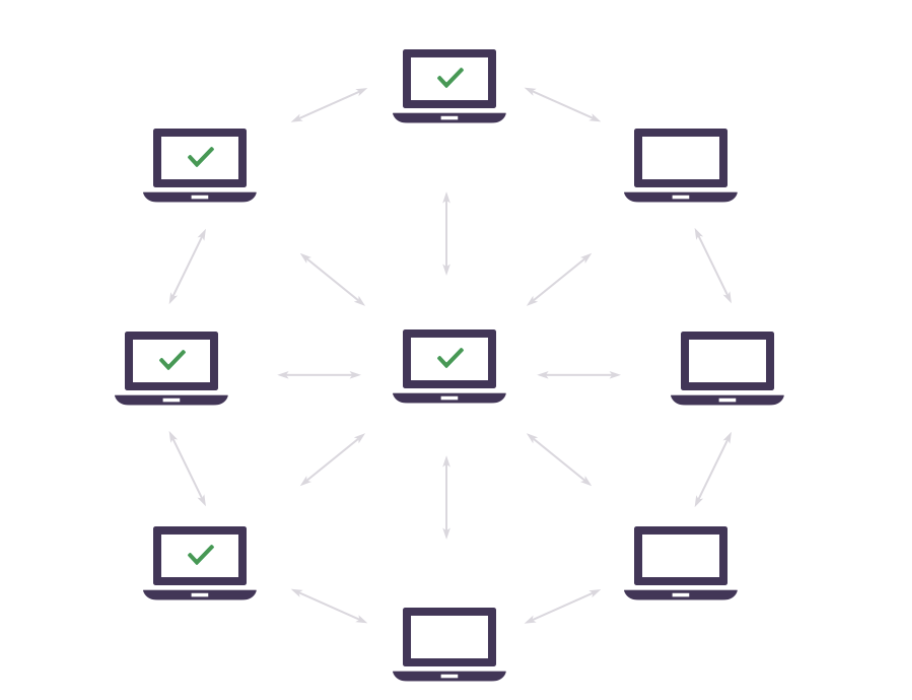

The transaction ledger on a blockchain, or distributed ledger technology, is a distributed database. This means it is publicly available as a reference. Think of the distributed or blockchain ledger as an encyclopedia of everything that has ever happened on the Excel sheet. The encyclopedia can be accessed as long as you have access to the internet.

However, the blockchain transaction ledger is continuously updated as new transactions are added. We will look at how new blocks are generated in more detail later. Knowing that a blockchain’s distributed ledger is constantly changing is essential. This also means there must be a system where one can always trust the latest encyclopedia version.

This is where the word distributed comes into play. Several nodes or users (more on this later) are responsible for securing the blockchain network and verifying new recorded transactions. All these nodes have a digital copy of the transaction ledger. Each time a new block is added to the blockchain, the ledger that records the previous blocks and transactions is updated across all nodes in the network.

Thus, a transaction ledger that is entirely public and decentralized has been created. One is independent of any intermediary or third party because the entire network has access to and can verify the latest version of the distributed ledger.

Pre-programmed rules on the blockchain

Pre-programmed rules on the blockchain If we continue with the Excel sheet metaphor, it is easy to explain how blockchains can differ. One can refer to the transaction ledger as the protocol for the individual blockchain. Here are the rules for the specific blockchain, the framework within which the whole blockchain protocol, or Excel sheet, can operate.

The founder, or programmer, decides what functions her private blockchain or Excel sheet will have. Developers can specify the formulas to use, how to generate new blocks, and the rules for the private blockchain network to follow. After programming these blockchain platforms and securing them with cryptographic principles, they will govern the entire public blockchain network’s daily operation once launched.

A standard rule for a cryptocurrency blockchain is the number of units of value the protocol allows to be mined. Cryptocurrency usually has a predetermined amount of units associated with it. The programming of the underlying blockchain mining protocol ensures that only this number is generated. For Bitcoin, for example, it is 21 million.

But there will also be other rules on a blockchain. The transaction ledger is the blockchain’s essential rulebook on which all transactions will be based. Therefore, it is also up to the blockchain developer and the designer to write the code so blockchain users see that the blockchain has the desired functionality for its project.

Blockchain, cryptocurrency, projects, and nodes

Finally, it’s helpful to briefly overview all the different terms often used in connection with blockchain. It’s easy to get confused, especially if you’re uncomfortable with all the technology. But to keep things organized, you can consider the following four components:

- Blockchain

As we have seen here, the blockchain is the underlying technology. This rulebook determines how something (a cryptocurrency, for example) should operate daily. So, you can think of the blockchain as the technology.

- Cryptocurrency

Cryptocurrency is the associated value of a blockchain. Some blockchains are designed only to drive decentralized and digital currencies like Bitcoin. Other blockchains have their cryptocurrency as part of more significant blockchain functionality.

- Blockchain projects

Think of blockchain projects as the companies or people behind a blockchain. These are the founders and entrepreneurs who come up with new ways to use the existing blockchain infrastructure. Ethereum, for example, is a blockchain project.

- Nodes

Nodes are easiest to think of as the users on the Bitcoin blockchain network – at least those who actively maintain the network, verify transactions, and mine new blocks. These people in the Bitcoin network are known as miners who receive rewards from the current blockchain’s cryptocurrency.

A Closer Look at How Blockchain Works in Practice

Understanding more about how blockchain works and the different components of the blockchain. It’s time to go deeper into how a blockchain operates daily. This technology is in high use today.

Generating new blocks

As the name suggests, a blockchain is a chain of blocks – you can think of them as building blocks. The blocks contain transaction information; the blockchain’s protocol determines the type of transaction. But if you have a chain of blocks, you must also be able to generate new ones. So, how are these new blocks created?

For this to happen, a new transaction must be requested. Say you want to sell 1 bitcoin and have the recipient’s address. This will go as follows:

- The request is sent out to the blockchain network.

- A miner (node) verifies the transaction and competes with other miners to add it to a block with other transactions.

- The miner solves a mathematical problem (a cryptographic task)

- The network of nodes verifies the miner’s work and confirms the transaction against the ledger.

- The block is added to the blockchain, and the transaction goes through each new block following the time stamp of the blockchain protocol. It is up to the miners to ‘race’ to solve the mathematical problem required to add the transactions into a new block. Miners are paid on their side in cryptocurrency.

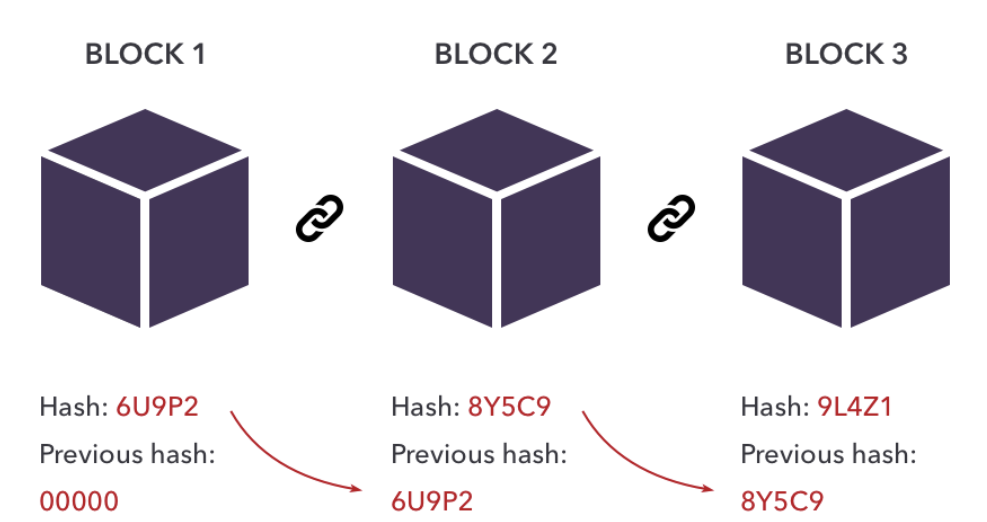

Block fingerprints and data

How can the Bitcoin network check that the new block matches the transaction ledger? Each new block contains transaction data – for example, how much bitcoin will be sent from Person A to Person B. However, a decentralized system requires some form of consensus-building; the nodes must be able to agree with each other.

This is where so-called hashes come into play. This can be compared to fingerprints or signatures; each new block in a blockchain has its hash. But in addition to this previous block’s unique hash, the previous block itself also contains the previous block’s hash. So, the new block’s signature points back to the last signature in the chain.

In the transaction ledger, all transactions, with their respective hashes, are publicly and readily available to the network participants and the general public. Send money in the form of cryptocurrency. Your transaction will have a unique cryptographic hash recorded in the distributed ledger public Excel sheet.

Note that the data content of a block does not necessarily need to be economic. We are moving toward other potential uses for the blockchain, which we will look at later in this guide.

Technically, a block can contain anything as long as it is digitized. It can be a transaction, information, part of a smart contract, or a vote. The hashes secure the transaction and are cryptographically locked into the blockchain. What power do nodes have over the types of blockchain networks used?

What power do nodes have over the blockchain?

As we saw in the example above, the users who secure the network, or the nodes, are responsible for the entire blockchain system. These people must secure the decentralized network by ensuring consensus; they use enormous data power to solve the blockchain system’s cryptographic tasks. In return, they get cryptocurrency.

As a result, one might also ask: If a relatively small group of people, compared to the total number of users, holds most of the power over a blockchain, can it truly be decentralized? For example, Bitcoin has struggled with large mining pools, which coordinate their processing power and thus win blocks more often than their smaller competitors.

Although this is a potentially problematic issue, it is essential to remember that the nodes on all blockchains have good motivation to do their job well. A small group gets a lot of power with large mining pools. Nevertheless, this does not mean they will misuse the blockchain in any way; otherwise, they will lose the reward for their effort.

From a decentralization perspective, however, all blockchains should strive to avoid a small percentage of the big cake holding power over the network. If not, you end up with centralization, where nodes cooperate to gain the most profit and thus capture an unfair market share.

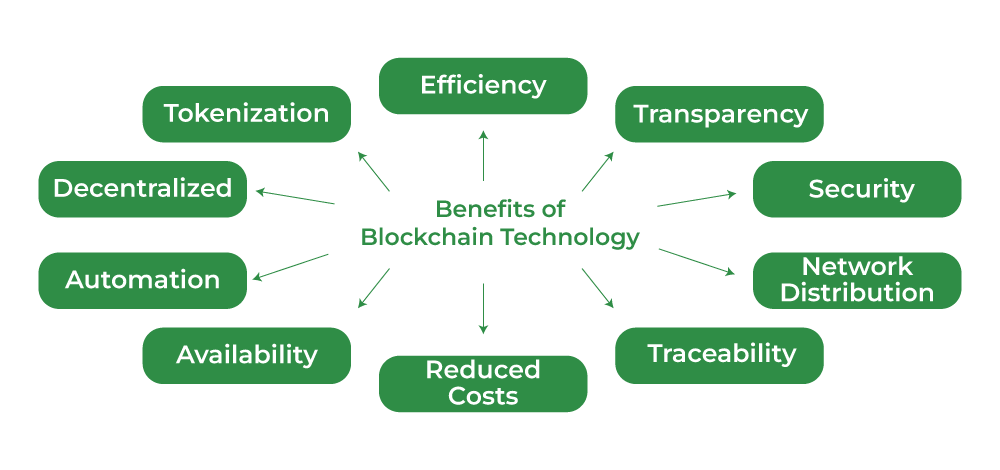

Blockchain strengths: The benefits of decentralization

Decentralization is sacred within blockchain technology. But what are the real benefits for you and me in everyday life with decentralizing services that are centralized today?

Waterproofed transactions – not only for money

We have already mentioned that the blockchain is secure. However, it is critical to specify precisely how to secure a blockchain implementation. And especially if we compare it to the services offered today. The two have a massive difference; the opposition centralization/decentralization makes this difference.

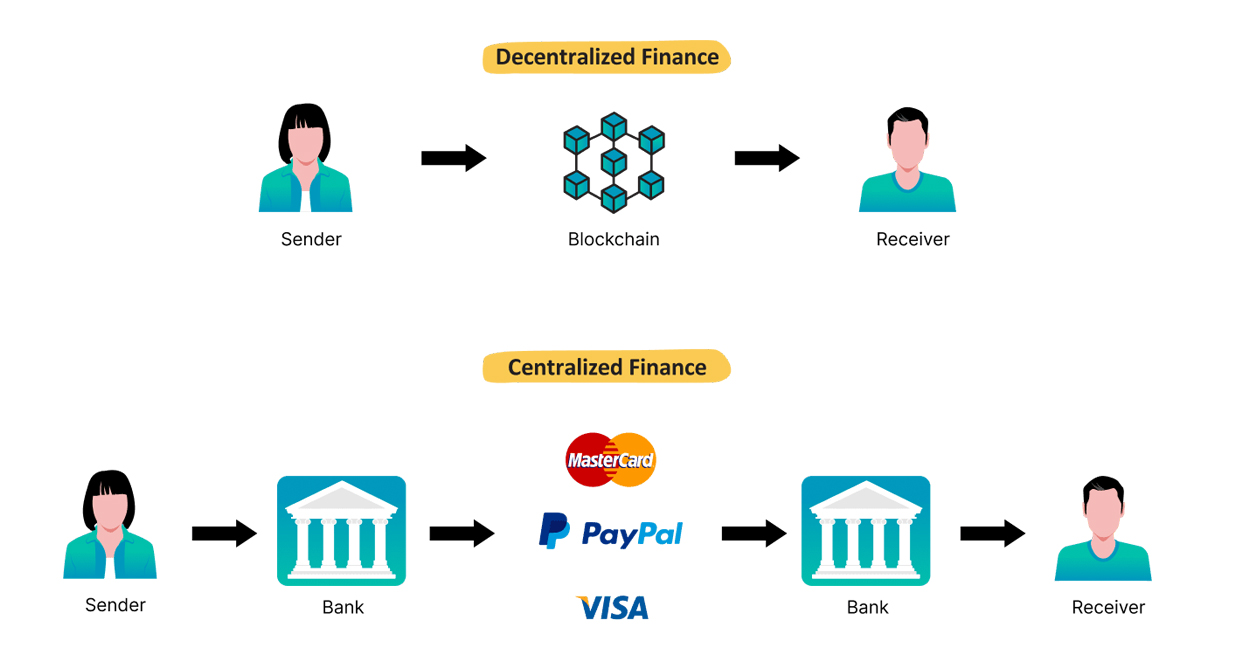

Imagine a traditional bank transaction. You send money from your bank account to a recipient’s account. All normal movement of funds occurs at your bank and the recipient’s bank.

This further means that all information in connection with the transaction is also located with these two banks. They are centralized. If someone wanted to attack your bank, they would only need to get through the security of this one centralized database.

The blockchain is something completely different.

We have already seen how a transaction is carried out here. The most crucial point concerning watertight transactions is:

- The network of nodes verifies the miner’s work and confirms the transaction against the ledger.

A whole network of nodes, all of which have their copy of the information from the transaction ledger, must confirm every transaction. Attacking a blockchain and doing any real damage means you not only have to get through the security of one database. You have to get through the safety of thousands of nodes’ computers.

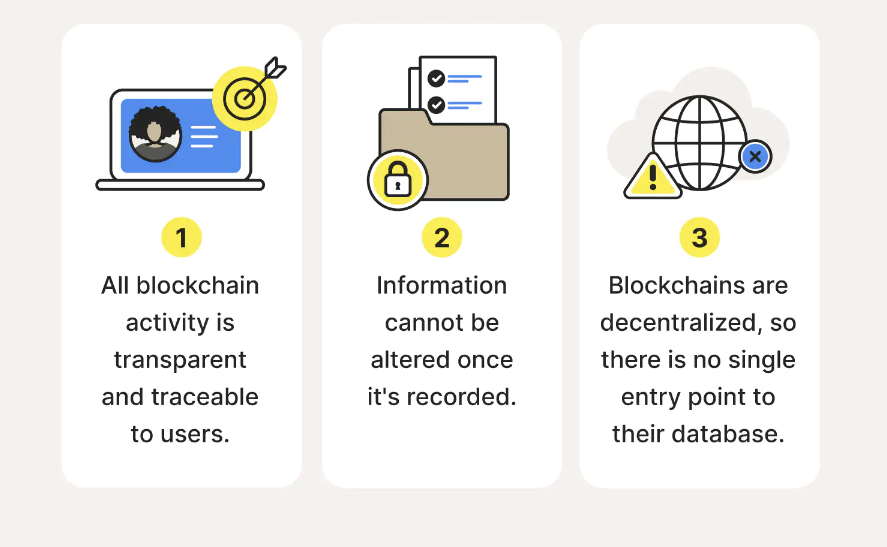

The security and transparency of a blockchain do not rely on intermediaries.

This level of security is groundbreaking when it comes to all digital assets and all digital currency transactions. Transactions on the blockchain, which are locked into a sequence and confirmed by thousands of individual users, provide exceptional security because they cannot be tampered with. This is because it would take an enormous effort to attack the blockchain successfully.

The second advantage of a decentralized transaction using distributed ledger technology is that it provides transparency, not in terms of names or faces, but because anyone with internet access can see all the transactions that have ever occurred on the blockchain.

This distributed ledger technology also provides transparency, leading to additional security because everyone can agree on what has happened on the blockchain historically.

Security and transparency are achieved without any need for intermediaries. This is called a trustless system in English, which does not rely on trust. As we saw earlier, a blockchain only requires faith in cryptography and programming. One is never dependent on trusting a third party to take care of their money or digital assets.

The network holds power, not a centralized authority.

In many ways, the nodes hold the power to validate transactions made on a public blockchain network. And if these nodes gather in too large numbers, one could have a problem in the form of, for example, large mining pools.

Nevertheless, the nodes are the network. We are talking about thousands of users who contribute to securing the public blockchain network’s transactions, storing data, and operations.

Therefore, the network holds power on a blockchain, not a centralized authority. One background of Bitcoin was the financial crisis in 2008, where banks had mismanaged their responsibility for customers’ money. On a blockchain, this problem doesn’t arise precisely because the security of the blockchain is directly related to the size of the network.

Everyone agrees on the history of fraudulent transactions, as it is public and available. Confirmed transactions cannot be tampered with, as they are an integral part of the public blockchain, with all new blocks connected to the previous ones. Furthermore, it is almost impossible (no one has succeeded) to break a blockchain or carry out any truly harmful attack.

The strength of blockchain technology lies in the size of the network, not the power of a centralized institution. And that has a lot to say in an increasingly globalized world, where it is becoming increasingly common to communicate and do business with each other across continents.

Trusted Partners

5.0

Fees

0.1 – 0.5%

Tradable Coins

600+

Payment Options

+ 3

4.7

Fees

0.01 – 0.10 %

Tradable Coins

100+

Payment Options

4.3

Fees

0.04% – 0.10%

Tradable Coins

145 +

Payment Options

What are the use cases of blockchains?

Blockchains are the technology that supports, for example, Bitcoin, which is a cryptocurrency. But does the potential of blockchains stop here? Are there other things that the technology can be used for?

Satoshi Nakamoto, Bitcoin, and the financial blockchain

From a historical development perspective, one can see various use cases of blockchain technology. The blockchain system as we know it today was invented by Satoshi Nakamoto and launched as Bitcoin in 2009. The technology was based on digital timestamps, which came almost 20 years earlier, in 1991. The main idea was irreversible transactions using a timestamp.

When Nakamoto launched Bitcoin, it was in the aftermath of the worldwide financial crisis of 2008. His or their vision (we still need to learn who Nakamoto is today) was about a decentralized payment system where one didn’t need to trust the banks that had let down the world economy.

In that sense, the first, and still the most significant, use case for blockchains was financial.

The technology served as the foundation for a payment system. And eventually, more and more payment systems with their private blockchains, such as Litecoin, came into play.

One could easily have imagined that technological development would have stopped here. But it didn’t. Remember that the transactions in blocks can contain anything. The decentralized blockchain network enables the movement of assets beyond just money.

Vitalik Buterin and Smart Contracts on the Blockchain

Ethereum blockchain was groundbreaking when launched, allowing developers to build their applications on top of the blockchain for the first time. Bitcoin only supports the transaction flow of a decentralized cryptocurrency. With Ethereum, one could suddenly develop blockchain applications and use the blockchain for anything they wanted.

Vitalik Buterin, the now 24-year-old Canadian-Russian programmer who conceived Ethereum, introduced what we now know as smart contracts. Smart contract contracts are based on if this, then that logic. This is the sequence that allows for programming a transaction flow with the security of the blockchain network.

In this way, one could suddenly have the blockchain do much more than transfer money from one wallet to another. As a blockchain developer, you can write programming code that validates transactions in sequence, such as ensuring Person A pays rent to Person B on the 15th of the month or automatically transferring ownership of a house’s private key when the money arrives in the account. Blockchain technology secures this process in the same manner as financial transactions.

Today, many applications have been built on top of the blockchain using Ethereum’s underlying programming. These are called dApps or decentralized applications. However, most enthusiasts and experts believe we have only seen a fraction of what the blockchain can do for us.

Securing Values: Potential Use Cases for the Blockchain

All transactions are eternal because blockchain technology is based on time stamping and sequencing. After a certain point in the blockchain, all transactions reference previous transactions, making them impossible to change or delete. Blockchain technology thus has enormous potential in securing values and maintaining watertight systems.

The blockchain can digitize any value. Imagine a world where your house is digitized, your car exists on the blockchain, and all the valuable items you own are secured by a decentralized network of thousands of blockchain nodes spread across the globe. This illustrates how many potential use cases exist in reality for the blockchain.

If everything can be digitized, one can see blockchain strategy to cut out intermediaries and vulnerable centralized databases in the business network of various industries. The future of blockchain technology is bright.

The future: How does blockchain technology look in the future?

Although it is up to the genuinely innovative programmers, entrepreneurs, and founders to lead the way to the future of blockchain technology, it is easy to imagine some of the possibilities if one lets the imagination run wild.

Decentralized Finance (DeFi)

Since its inception, blockchain technology has had the greatest impact on the finance sector, particularly in the form of cryptocurrency. Therefore, it is unsurprising that this sector has already begun to embrace the new technology and open up to decentralization based on private blockchain networks and blockchain networks.

Several cryptocurrency projects have partnered with central banks to develop new payment systems and services. Furthermore, several major banks and financial institutions have partnered with various blockchain companies and platforms to find solutions for integrating blockchain technology with traditional banking systems.

Given how much cryptocurrency has grown and continues to grow, there is a high probability that consumers worldwide will want this type of technology. The development of blockchain technology will impact the finance sector, and those who actively work towards consolidating the centralized and decentralized are likely to be the winners.

Globalization and digital values across world continents

What if anyone could digitalize any value and sell it to anyone else – anywhere in the world? This is precisely what blockchain technology makes possible. The transaction ledger is a decentralized network. Thousands of nodes secure multiple transactions on the network.

Let’s say you digitalized your house on the blockchain platform. All official papers on the house came as part of the package. So, anyone in the world could see the history and value of the property. Let’s now say you wanted to sell your house. With blockchain technology, you can do this to anyone in the world.

Of course, certain things need to be in place for this type of situation to become a reality. Identity verification through a private blockchain database is one thing. Blockchain networks set up within systems under regulations and governments are another. But if we could merge blockchain technology with the social systems we have today, world trade would look very different.

Blockchain for identity, political elections, homeownership, and virtual reality

It is valid for all social structures we already use. Isn’t it safer to confirm identity with a waterproof network? Hold legitimate, uncorrupted political elections? Confirm homeownership, or land ownership, in areas with much conflict and unrest. Or do all this and more in virtual reality?

Blockchain technology enthusiasts firmly believe its applications will expand into many areas of daily life. Developers work on groundbreaking projects to identify sectors and structures suitable for implementing blockchain technology. Often, it makes existing systems even better.

As long as cryptography is strong enough, only the imagination limits what blockchain technology can do. With a strong network, timestamping, and consensus on all transactions, one can imagine an entire society secured and operated by blockchain technology.

Summary

Blockchain technology is a digital ledger that records transactions decentralized and securely. Satoshi Nakamoto invented it in 2009, and it has been used to create digital currencies like Bitcoin.

Blockchain technology can be utilized for purposes beyond financial transactions. Vitalik Buterin introduced smart contracts to the blockchain, allowing blockchain developers to program a sequence of transactions. Today, many applications have been built on top of the blockchain using Ethereum’s programming.

Blockchain has enormous potential in securing values and maintaining watertight systems. Since transactions on the blockchain are irreversible and eternal, blockchain technology can digitize any value. Utilizing blockchain’s decentralized and transparent nature, various industries can potentially eliminate intermediaries and vulnerable centralized databases in their business networks.

The financial sector has embraced blockchain technology and has partnered with various blockchain companies and platforms to find solutions for integrating blockchain technology with traditional banking systems. Blockchain technology can also have applications in identity verification, political elections, homeownership, and virtual reality. As long as cryptography is strong enough, only imagination limits what blockchain technology can do.

Blockchain is a decentralized digital ledger of transactions stored on computers connected through the internet. It consists of blocks containing transaction data linked together chronologically into chains that cannot be altered or deleted once added, making the blockchain an accurate way to track and verify transactions.

Blockchain technology enables secure and transparent record-keeping of transactions. One such use case is in Bitcoin blockchain technology which acts like a decentralized public ledger to record all cryptocurrency transactions.

Blockchain technology can be utilized for many purposes, including creating decentralized networks, secure record keeping, executing smart contracts, and verifying digital identities. Applications exist across finance, supply chain management, and digital identity verification industries.

No, blockchain technology does not represent a cryptocurrency. It is used as the basis for supporting other cryptocurrencies like Bitcoin. But blockchain can also be utilized for non-crypto applications, like creating secure digital records or executing smart contracts.